What is the 10 20 rule personal finance?

It says your total debt shouldn't equal more than 20% of your annual income, and that your monthly debt payments shouldn't be more than 10% of your monthly income. While the 20/10 rule can be a useful way to make conscious decisions about borrowing, it's not necessarily a useful approach to debt for everyone.

While it's technically a rule of thumb as opposed to an enforceable decree, the 10/20 rule is a system of budgeting that can work for virtually anyone. The idea is to keep your total debt at or under 20% of your annual income, while maintaining monthly payments at no more than 10% of your monthly net income.

The 70-20-10 budget formula divides your after-tax income into three buckets: 70% for living expenses, 20% for savings and debt, and 10% for additional savings and donations. By allocating your available income into these three distinct categories, you can better manage your money on a daily basis.

What does this mean exactly? This means that total household debt (not including house payments) shouldn't exceed 20% of your net household income. (Your net income is how much you actually “bring home” after taxes in your paycheck.) Ideally, monthly payments shouldn't exceed 10% of the NET amount you bring home.

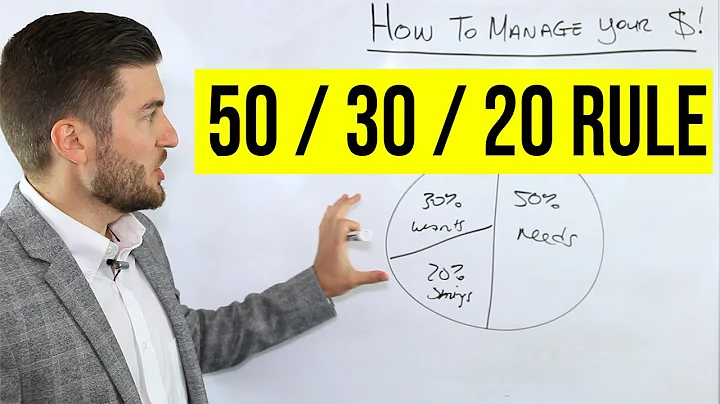

Key Takeaways. The 50/30/20 budget rule states that you should spend up to 50% of your after-tax income on needs and obligations that you must have or must do. The remaining half should be split between savings and debt repayment (20%) and everything else that you might want (30%).

The most common way to use the 40-30-20-10 rule is to assign 40% of your income — after taxes — to necessities such as food and housing, 30% to discretionary spending, 20% to savings or paying off debt and 10% to charitable giving or meeting financial goals.

30/30/40. Thirty percent of your income goes toward housing expenses, 30% toward other living costs like food and transportation, and 40% toward discretionary spending and savings.

#1 Don't Spend More Than You Make

When your bank balance is looking healthy after payday, it's easy to overspend and not be as careful. However, there are several issues at play that result in people relying on borrowing money, racking up debt and living way beyond their means.

YOUR BUDGET

The 80/20 budget is a simpler version of it. Using the 80/20 budgeting method, 80% of your income goes toward monthly expenses and spending, while the other 20% goes toward savings and investments.

Those will become part of your budget. The 50-30-20 rule recommends putting 50% of your money toward needs, 30% toward wants, and 20% toward savings. The savings category also includes money you will need to realize your future goals. Let's take a closer look at each category.

What are the 3 C's of credit?

The factors that determine your credit score are called The Three C's of Credit – Character, Capital and Capacity.

Character, capital (or collateral), and capacity make up the three C's of credit. Credit history, sufficient finances for repayment, and collateral are all factors in establishing credit.

The rule dictates that total consumer debt shouldn't exceed 20% of your annual take-home pay and monthly debt payments shouldn't exceed 10% of your monthly take-home pay. This rule of thumb can help consumers cap the amount of debt they hold, which is important for their financial health and their credit score.

Are you approaching 30? How much money do you have saved? According to CNN Money, someone between the ages of 25 and 30, who makes around $40,000 a year, should have at least $4,000 saved.

The rule of 25 is simple: You should have 25 times the annual amount you plan to spend in retirement saved before you leave the workforce.

Consider an individual who takes home $5,000 a month. Applying the 50/30/20 rule would give them a monthly budget of: 50% for mandatory expenses = $2,500. 20% to savings and debt repayment = $1,000.

The Rule of 120 (previously known as the Rule of 100) says that subtracting your age from 120 will give you an idea of the weight percentage for equities in your portfolio.

One frequently used rule of thumb for retirement spending is known as the 4% rule. It's relatively simple: You add up all of your investments, and withdraw 4% of that total during your first year of retirement.

At least 20% of your income should go towards savings. Meanwhile, another 50% (maximum) should go toward necessities, while 30% goes toward discretionary items. This is called the 50/30/20 rule of thumb, and it provides a quick and easy way for you to budget your money.

What Is the 75 15 10 Rule and How Does It Work? The 75/15/10 rule is a simple way to budget: Use 75% of your income for everyday expenses, 15% for investing and 10% for saving. It's all about creating a balanced and practical plan for your money.

What is the 50 15 5 rule?

50 - Consider allocating no more than 50 percent of take-home pay to essential expenses. 15 - Try to save 15 percent of pretax income (including employer contributions) for retirement. 5 - Save for the unexpected by keeping 5 percent of take-home pay in short-term savings for unplanned expenses.

The 10% rule of investing states that you must save 10% of your income in order to maintain a comfortable lifestyle during retirement. This strategy, of course, isn't meant for everyone as it doesn't account for age, needs, lifestyle, and location.

I refer to these as the “Five Ps” of business success: Product, Pricing, People, Process, and Planning. These foundational elements encompass the resources critical to a strategic plan that prioritizes factors to move your company forward, maintain positive cash flow, and create an environment for growth.

Golden Rule #1: Don't spend more than you earn

Understand the difference between needs and wants, live within your income, and don't take on any unnecessary debt.

The Pareto principle states that for many outcomes, roughly 80% of consequences come from 20% of causes. In other words, a small percentage of causes have an outsized effect. This concept is important to understand because it can help you identify which initiatives to prioritize so you can make the most impact.